When reviewing documents with real estate clients, title insurance is one of the most asked-about costs on the settlement statement. During the process, you will learn there are two types of title insurance policies, an Owner’s title insurance and a Lender’s title insurance. What are they and who pays for them?

Title insurance is a type of insurance that protects real estate buyers and mortgage originators (lenders) against potential losses due to issues with the title to a property. The “title” is the legal ownership rights to the property. The title says who actually owns the property. Some common issues where title insurance would be used is forged documents, unpaid taxes, errors in public records, and boundary disputes.

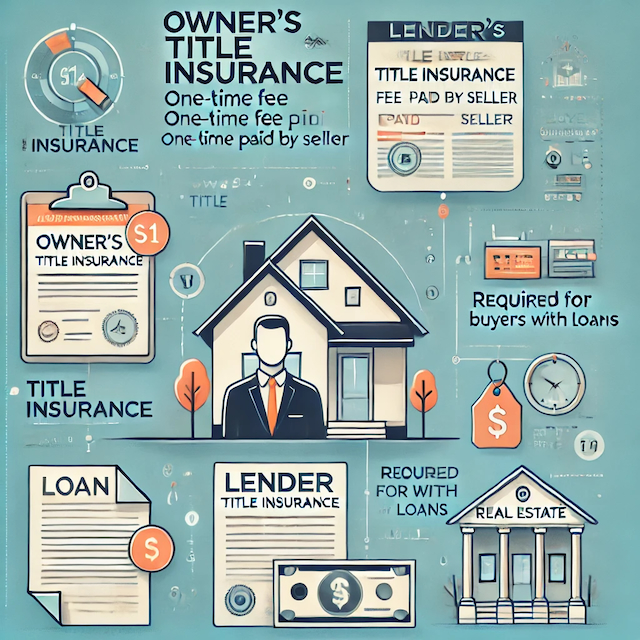

On closing day, as we go through the real estate documents, you will notice on your settlement statement that you are being charged for one of two different types of title insurance, depending on if you are the seller or the buyer in the transaction. The seller of the property pays for the Owner’s title insurance policy and the buyer of the property pays for the Lender’s title insurance policy.

Owner’s title insurance, often called an Owner’s Policy, is a one-time flat fee that the seller pays to the title insurance company for the benefit of the buyer. Although it is only a one-time payment, the insurance policy lasts as long as the buyer owns the property. The buyer will receive the Owner’s title insurance policy as stated in terms for the amount of the sale price after the closing and it will list all of the benefits and restrictions of the policy. If you are the buyer, do not lose this policy; you will need it if you need to file a claim against your title insurance policy at some point in the future.

Lender’s title insurance, also known as a Loan Policy, is based on the actual dollar amount on the loan or mortgage. If you are the buyer, your lender will require you to purchase a Lender’s title insurance policy to protect the lender from potential claims of prior third parties that may be senior to the lender’s secured interest in the property. What this means is that, as a buyer, you must pay as part of your closing costs so the title company will issue a title insurance policy to your lender. This is how your lender protects its interest in your property. Are you required to purchase this policy? Well, you will not be able to get the loan without it. If you buy the property in cash, you will not have to get a lender’s title insurance policy.

Both of these charges are non-negotiable items that buyers and sellers will find on the closing statement. It could be a high-cost item but gives the buyer and lender extra protection for their investment.

Lender’s title insurance, also known as a loan policy, is based on the actual dollar amount on the loan or mortgage. If you are the buyer, your lender will require you to purchase a lender’s title insurance policy to protect the lender from potential claims of prior third parties that may be senior to the lender’s secured interest in the property. What this means is that, as a buyer, you have to pay as part of your closing costs so that the title company will issue a title insurance policy to your lender. The bank is protecting their money. Are you required to purchase this policy? Well, you will not be able to get the loan without it. If you buy the property in cash, you will not have to get a lender’s title insurance.

Both of these charges are non-negotiable items that buyers and sellers will find on the closing statement. It could be a high-cost item but gives the buyer and lender extra protection for their investment. Please contact us if you have any questions about your real estate transaction.